A fraudulent transfer claim is a civil lawsuit that enables creditors to reverse asset transfers made to avoid debt repayment, either through intentional deceit or unfair value exchanges during insolvency. Formally called a “fraudulent conveyance” in older legal texts, this remedy exists under both federal bankruptcy law and state statutes, most notably the Uniform Voidable Transactions Act (UVTA). If someone owes you money and moves assets to a family member, sells property far below market value, or shifts funds offshore before you can collect, a fraudulent transfer claim is your legal mechanism to undo that transfer and recover what you are owed.

What constitutes a fraudulent transfer under U.S. law?

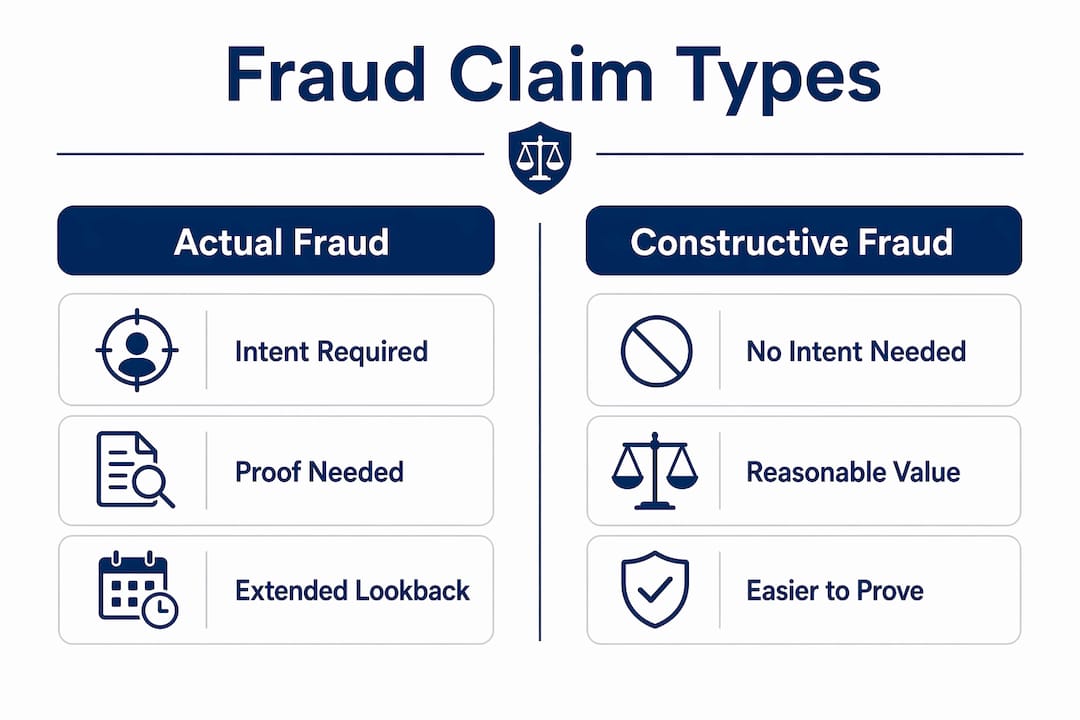

A fraudulent transfer occurs when a debtor moves assets in a way that harms creditors, either through deliberate intent or through an economically unfair transaction during financial distress. U.S. law recognizes two distinct theories: actual fraud and constructive fraud. Both are governed by 11 U.S.C. § 548 in bankruptcy and by state UVTA statutes outside of bankruptcy.

Actual fraud requires proof that the debtor transferred assets with the specific intent to hinder, delay, or defraud creditors. Because intent is rarely admitted, courts rely on circumstantial evidence called “badges of fraud.” These include:

- Transfers to insiders such as family members or business partners

- Transfers made while litigation was pending or threatened

- Transfers of substantially all of the debtor’s assets

- Concealment of the transfer or the assets involved

- Transfers made for little or no consideration

Constructive fraud does not require proof of intent. Instead, courts ask two questions: Did the debtor receive reasonably equivalent value for the transfer? Was the debtor insolvent at the time, or did the transfer render them insolvent? A classic example is selling a $400,000 property for $50,000 while carrying significant debt. That transaction is textbook constructive fraud regardless of what the debtor claims their intent was.

The burden of proof in both theories is preponderance of the evidence. This means you need to show it is more likely than not that the transfer was fraudulent. That is a far lower bar than the “beyond a reasonable doubt” standard in criminal cases, which makes civil fraudulent transfer claims accessible to most creditors.

Lookback periods matter significantly. Federally, transfers are voidable within 2 years of a bankruptcy filing. Under state UVTA laws, that window extends to 4 years, and a discovery rule can reset the clock if the transfer was concealed.

How do actual fraud and constructive fraud differ in fraudulent transfer claims?

The core difference between actual fraud and constructive fraud is what you must prove. Actual fraud demands evidence of subjective intent. Constructive fraud demands evidence of objective economic harm.

| Feature | Actual fraud | Constructive fraud |

|---|---|---|

| Intent required | Yes, must prove debtor meant to defraud | No, focuses on economic reality |

| Key question | Did the debtor intend to hinder creditors? | Did the debtor receive fair value while insolvent? |

| Evidence needed | Badges of fraud, communications, timing | Financial records, appraisals, insolvency proof |

| Difficulty of proof | Higher, subjective standard | Lower, objective standard |

| Common use case | Asset concealment, insider transfers | Below-market sales, gifts during insolvency |

Constructive fraud claims are the focus for most creditor attorneys precisely because they remove the nearly impossible task of reading a debtor’s mind. If a debtor transferred a business interest to a sibling for $1 while carrying $2 million in debt, you do not need to prove the debtor “meant” to cheat you. The numbers speak for themselves.

Actual fraud claims carry a strategic advantage, though. A successful actual fraud finding can extend the lookback period and may support additional remedies. Courts in cases involving Celsius, Terraform Labs, and similar crypto insolvencies have used actual fraud theories to pursue transfers made years before collapse.

Pro Tip: If you are unsure which theory applies to your situation, start by gathering all financial records from the 4 years before the transfer. Constructive fraud is almost always easier to establish, but the documents may reveal intent evidence that strengthens an actual fraud claim as well.

What legal remedies and outcomes can creditors expect?

Courts can undo fraudulent transfers through several distinct remedies, all civil in nature. The goal is restoration, not punishment. Here is what a successful fraudulent transfer claim can produce:

- Avoidance of the transfer. The court voids the transaction entirely, returning the asset to the debtor’s estate where creditors can reach it.

- Monetary judgment against the transferee. If the asset cannot be returned (for example, it was sold to a third party), the court can order the transferee to pay the asset’s value in cash.

- Injunctions and asset freezes. Courts can issue orders preventing further transfer or dissipation of assets while the case is pending.

- Appointment of a receiver or trustee. In complex cases, courts appoint a neutral party to manage and preserve assets. Murphyslawcrypto has experience with court-appointed receivers in crypto fraud disputes where assets span multiple wallets and exchanges.

- Trustee actions in bankruptcy. A bankruptcy trustee can pursue fraudulent transfer claims on behalf of all creditors, which reduces individual litigation costs and consolidates recovery efforts.

These remedies are civil, not criminal. A fraudulent transfer claim does not send anyone to prison. However, a successful civil judgment can be the foundation for a separate criminal referral if the evidence reveals deliberate fraud at scale.

The practical value of these remedies is significant. Courts can undo fraudulent transfers through avoidance orders, injunctions, and receiverships, restoring creditors’ ability to collect on debts they were otherwise blocked from reaching. In crypto fraud cases, where assets move across blockchains in seconds, injunctions and receiver appointments are often the most critical tools available.

How can you file and pursue a fraudulent transfer claim?

Filing a fraudulent transfer claim requires methodical preparation. The steps below apply whether you are pursuing a claim in state court under the UVTA or in federal bankruptcy court under 11 U.S.C. § 548.

-

Identify the suspicious transfer. Look for asset movements that coincide with your debt arising, litigation being filed, or the debtor’s financial decline. Timing is the first indicator courts examine.

-

Gather financial records. Obtain bank statements, property records, corporate filings, and tax returns covering the relevant lookback period. Forensic accountants are critical here. They can reconstruct a debtor’s financial condition at the time of the transfer and establish insolvency.

-

Determine the defendants. You must name both the debtor and the transferee. Naming the transferee is not optional. Transferees frequently claim they acted in good faith, but courts reject that defense when a reasonable person would have recognized red flags such as a below-market price or an unusual relationship to the debtor.

-

Assess the statute of limitations. The general rule is 4 years with a 1-year discovery extension under state UVTA laws. If the transfer was concealed, the discovery rule may reset the clock from the date you learned of the transfer, not the date it occurred.

-

File the complaint. Your attorney drafts a complaint alleging actual fraud, constructive fraud, or both. Pleading both theories is common because the evidence may support one more strongly than the other as the case develops.

-

Anticipate transferee defenses. Good faith is the most common defense. The transferee argues they paid fair value and had no knowledge of fraud. Your job is to show that objective red flags existed that a reasonable buyer would have investigated.

Pro Tip: Do not wait to consult an attorney. The statute of limitations in fraudulent transfer cases runs from the transfer date, not from when you discovered the harm. Every month of delay narrows your legal window.

Asset protection planning is legal up to a point. It becomes fraudulent only when it involves deception after a claim arises or transfers designed to avoid known debts. If the debtor moved assets before any debt existed, your claim becomes significantly harder to prove.

Key takeaways

A fraudulent transfer claim is the most direct legal tool available to creditors who have been blocked from collecting a debt by a debtor’s deliberate or economically unfair asset transfers.

| Point | Details |

|---|---|

| Two theories of liability | Actual fraud requires intent; constructive fraud requires only proof of unfair value and insolvency. |

| Lookback periods | Federal law covers 2 years; state UVTA laws extend coverage to 4 years with a discovery extension. |

| Civil remedies available | Courts can void transfers, freeze assets, appoint receivers, or issue monetary judgments against transferees. |

| Name the transferee | Failing to name the transferee as a defendant is the most common filing mistake and can sink an otherwise strong claim. |

| Act quickly | The statute of limitations runs from the transfer date, so delay directly reduces your legal options. |

Why constructive fraud is the claim most creditors should file first

Most creditors I speak with assume they need to prove the debtor deliberately cheated them. That assumption leads them to spend months chasing emails, text messages, and witness statements trying to establish intent. In the majority of cases, that effort is unnecessary.

The shift from “fraudulent conveyance” to “voidable transaction” under the UVTA reflects exactly this reality. Modern fraudulent transfer law is designed around economic outcomes, not moral judgments. If the debtor transferred a valuable asset for far less than it was worth while carrying debt they could not pay, the law presumes harm to creditors regardless of what the debtor claims they intended.

Where I see creditors lose otherwise winnable cases is in two places. First, they fail to name the transferee as a defendant, which lets the asset stay transferred even if the debtor is found liable. Second, they underestimate the good faith defense. A transferee who paid some consideration, even if below market, will argue they acted reasonably. You need transaction evidence, pricing comparisons, and relationship evidence to defeat that argument.

The other misconception worth addressing is timing. Many creditors believe that if they did not discover the transfer immediately, their claim is gone. The discovery rule exists precisely to address concealed transfers. If the debtor hid the transaction, courts will often measure the limitations period from the date you could reasonably have discovered it, not the date it occurred.

If you have lost money to a fraudulent transfer in a crypto context, the legal tools available to you are the same as in any civil case, but the evidence gathering is more complex. Blockchain records, exchange data, and wallet tracing require specialized expertise that general civil litigators often lack.

— Mark

How Murphyslawcrypto can help you recover assets

Fraudulent transfer claims in crypto cases are among the most technically demanding in civil litigation. Assets move across blockchains in minutes, transferees operate through pseudonymous wallets, and debtors exploit jurisdictional gaps to delay recovery.

Murphyslawcrypto is a licensed law firm with active courtroom experience in crypto fraud recovery, including matters involving Celsius, Terraform Labs, and BitMEX. Liam Murphy, Esq. (Penn Law, formerly Paul Hastings and McKool Smith) leads a litigation team that knows how to trace assets on-chain, name the right defendants, and defeat good faith defenses in court. If you believe assets were fraudulently transferred to avoid a debt you are owed, explore your legal recovery options or review the firm’s fraud recovery litigation practice to understand how a real courtroom attorney approaches these claims.

FAQ

What is the fraudulent conveyance definition in simple terms?

A fraudulent conveyance, now more commonly called a voidable transfer, is any transfer of assets made to prevent creditors from collecting a debt. Courts can reverse these transfers through civil litigation.

How long do you have to file a fraudulent transfer claim?

The statute of limitations is generally 4 years under state UVTA laws, with a 1-year extension if the transfer was concealed. Federal bankruptcy law sets a 2-year lookback period.

What is the difference between fraud and fraudulent transfer?

Fraud is a broad category of intentional deception for financial gain. A fraudulent transfer is a specific civil claim targeting asset movements designed to put property beyond a creditor’s reach, and it does not always require proof of intent.

Can a bankruptcy trustee file a fraudulent transfer claim for me?

Yes. A bankruptcy trustee has the authority to pursue fraudulent transfer claims on behalf of all creditors in a bankruptcy case, which can reduce individual legal costs significantly.

What are common examples of fraudulent transfer in crypto cases?

Common examples include transferring cryptocurrency to a family member’s wallet before a judgment, selling digital assets to an insider at far below market value, and moving funds offshore through shell wallets to obscure ownership during active litigation.

Recommended

- Crypto Fraud Recovery: Your Legal Options Explained | Murphy’s Law Crypto

- Crypto Fraud: The Complete Legal Guide | Murphy’s Law Crypto

- What To Do If You’ve Been Scammed With Cryptocurrency: A Step-by-Step Legal Guide – Murphy’s Law – Crypto Law Firm

- Crypto Fraud Recovery Litigation – Murphy’s Law – Crypto Law Firm